How to Read Your CIBIL Report and Understand Every Section?

Most people download their CIBIL report for one reason — to check the score.

They see 780, feel happy, and close the file.

But that’s not how banks read your report.

When a bank officer opens your CIBIL report, the score is the last thing they look at. First, they go through the details that tell the real story — your personal information, your loan history, your payment behaviour, and certain remarks that can quietly destroy your chances of getting approved.

If you have ever wondered why someone with a 780 score still gets a loan rejected, the answer is almost always hidden somewhere inside the report.

This guide will help you read your CIBIL report exactly the way lenders read it.

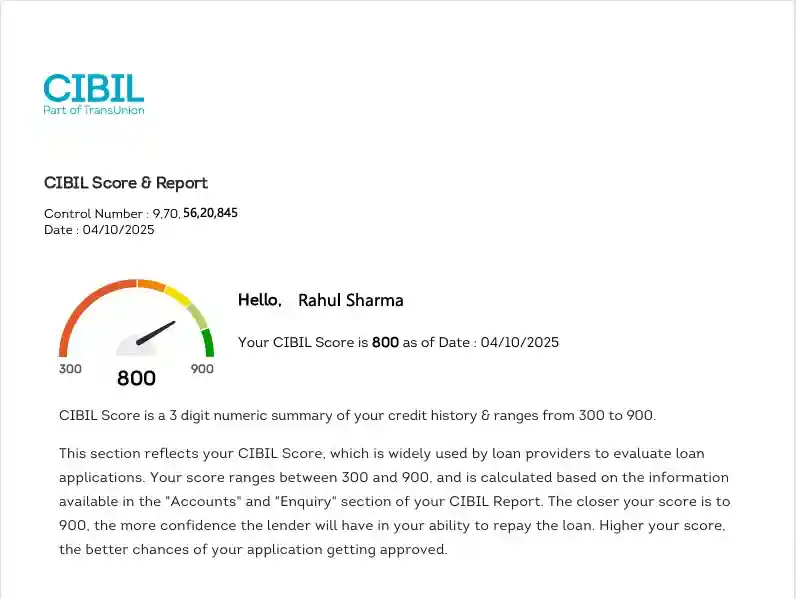

The First Page — More Than Just the Score

The first step is to download your CIBIL report from the TransUnion CIBIL official website. For help, you may refer to our post: How to Download Your Free CIBIL Report

At the very top, you see three things:

- Your CIBIL score

- A control number

- The date of the report

The control number is like the reference ID of this report. If you ever raise a dispute, this number is used to identify the exact report.

Your score, which ranges from 300 to 900, is simply a summary of everything that follows. A score of 800 is excellent, but it is only a reflection of the details that come later in the document.

The real information begins after this page.

Personal Details — Where Identity Confusion Starts

This section looks simple. It shows your name, date of birth, and gender.

But this is where many problems begin.

If your name is spelled slightly differently from your PAN records, or if the date of birth is wrong, banks may face difficulty verifying you. These small errors can delay loan approvals or trigger extra verification checks.

Identification Details — The PAN Connection

Next, you see different identification documents linked to your profile — PAN, Voter ID, Driving License, and sometimes even Ration Card details.

Out of all these, PAN is the most important.

Your entire credit history is built around your PAN number. If this is incorrect, or if another person’s loan is linked to your PAN, your report becomes unreliable. This is one of the most serious errors people discover when they read this section properly.

This is the first place you should check carefully.

Address Details — Your History of Residences

This part often surprises people.

You may see addresses you lived at 10 years ago, office addresses, or rented houses you have long forgotten.

This happens because banks report the last known address they had when you opened an account. Seeing old addresses is normal. But seeing an address you never lived at is not.

That is a sign that someone may have used your details.

Contact and Email Details — Silent Red Flags

Here you will find old mobile numbers and email IDs that you gave to banks while applying for loans or credit cards.

If you notice a number that you don’t recognize, it could mean your details were used somewhere without your knowledge.

Most people skip this section, but lenders don’t.

Employment Details — A Small but Important Entry

This simply shows whether you were marked as salaried or self-employed when you applied for credit. It may look minor, but it helps banks understand your financial profile.

The Heart of the Report — All Accounts

This is where banks spend most of their time.

Every loan and credit card you ever had, whether open or closed, is listed here. And each account has detailed information that tells lenders how you handled your credit.

You will see the bank’s name, the type of loan, when it started, how much was sanctioned, the current balance, and the EMI amount.

But lenders don’t stop here. They go deeper.

Account Details — What Banks Observe Carefully

When a bank reads this section, they mainly focus on a few lines:

- Current balance

- Amount overdue

- Date of last payment

- Date reported

- EMI amount

If the “Amount Overdue” field is not blank, it immediately raises concern.

They also check how recently the bank updated this account. If it hasn’t been updated for months, it may signal an issue.

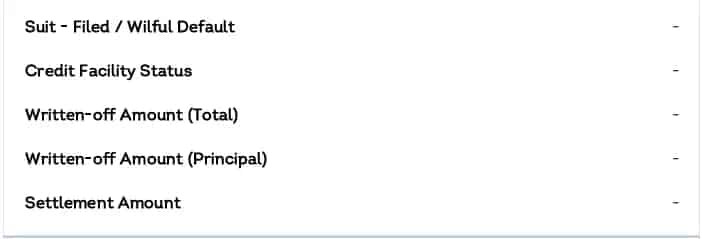

Credit Facility Status — The Line That Can Destroy Your Chances

In many reports, this field is blank. That is good.

But if this line shows anything else, it becomes very serious.

If it says Settled, it means you did not pay the full loan. You negotiated and paid less. Banks consider this almost like a default.

If it says Written-off, the bank has declared the amount as a loss.

If it says Suit Filed, legal action was taken.

If it says Post (WO) Settled, the loan was first written off and then partially paid.

These remarks stay for years and affect loan approvals even when your score looks good.

Written-off Amount — Hidden Trouble

If you see values in “Written-off Amount (Total)” or “Written-off Amount (Principal)”, it means the bank has already declared part of your loan as unrecoverable.

Even if you later repay the loan, this mark remains unless corrected.

Payment Status — Your Month-by-Month Behaviour (DPD Explained)

This is the most closely examined part of your report.

Here, every month is marked with a code that tells lenders exactly how you handled your EMI or credit card bill during that period. You may see terms like STD, SMA, SUB, DBT, or numbers such as 030, 060, 090.

At the core of this section is something called DPD — Days Past Due.

DPD is the actual number of days you were late in making that month’s payment.

- STD (Standard) → Paid on time (DPD = 000). This is ideal.

- 030 → 30 days late

- 060 → 60 days late

- 090 → 90 days late

- SMA (Special Mention Account) → Early warning stage before turning into a serious default

- SUB (Sub-standard) → Account has remained overdue for a long period

- DBT (Doubtful) → High probability of non-recovery

- LSS (Loss) → Considered non-recoverable by the lender

Even one 030 entry can make lenders cautious.

But when the report shows DPD values above 90 days (like 090, SUB, DBT, or LSS), it becomes a major red flag, especially for unsecured loans such as personal loans and credit cards. Many lenders — particularly PSU banks — treat this very seriously because it indicates a pattern of repayment stress.

Banks don’t just look at your score here. They read this section line by line, month after month, to judge your financial discipline.

A long stretch of STD (000 DPD) builds trust. A few high DPD months can undo years of good history.

Collateral and Legal Status

For secured loans, you may see property value and collateral type.

If “Suit Filed” or “Wilful Default” appears here, it is a legal warning sign for lenders.

Enquiry Details — Why Too Many Applications Hurt

At the bottom, you will see enquiry details.

This shows which banks checked your report and for what purpose.

If many banks checked your report in a short time, lenders assume you are aggressively trying to get loans. This reduces trust.

How Banks Actually Read Your Report

Banks don’t start with the score.

They check:

- Credit Facility Status

- Payment History

- Overdue amounts

- Written-off or settled remarks

- Enquiry count

Only after this do they glance at the score.

Why You Must Read the Full Report

Many people have excellent scores but hidden remarks like “Settled” or old late payments they never noticed.

These small lines are what cause loan rejections.

Reading the full report once a year helps you catch problems before banks do.

Final Thought

Your CIBIL report is not just a document. It is your financial reputation.

When you learn to read it properly, you stop guessing why loans get rejected. You start seeing your credit profile the same way lenders see it.

And once you understand this report, you will never look at your credit score alone again.

0 Comments

No comments yet. Be the first to share your thoughts!